Drone Business Insurance: Protect Your Aerial Enterprise

- Paul Simmons

- May 1, 2025

- 14 min read

Understanding Drone Business Insurance Essentials

Running a drone business requires careful planning, and a key part of that is securing the right insurance. Understanding drone business insurance can seem complicated, but it's essential for protecting your investment and ensuring your business thrives. Just like a pilot checks their aircraft before takeoff, you need to understand your insurance coverage.

Key Coverage Types

Drone operations face unique risks that standard business insurance often doesn't cover. Specialized policies address the specific challenges of using Unmanned Aerial Vehicles (UAVs) commercially. Here are some key coverage types to consider:

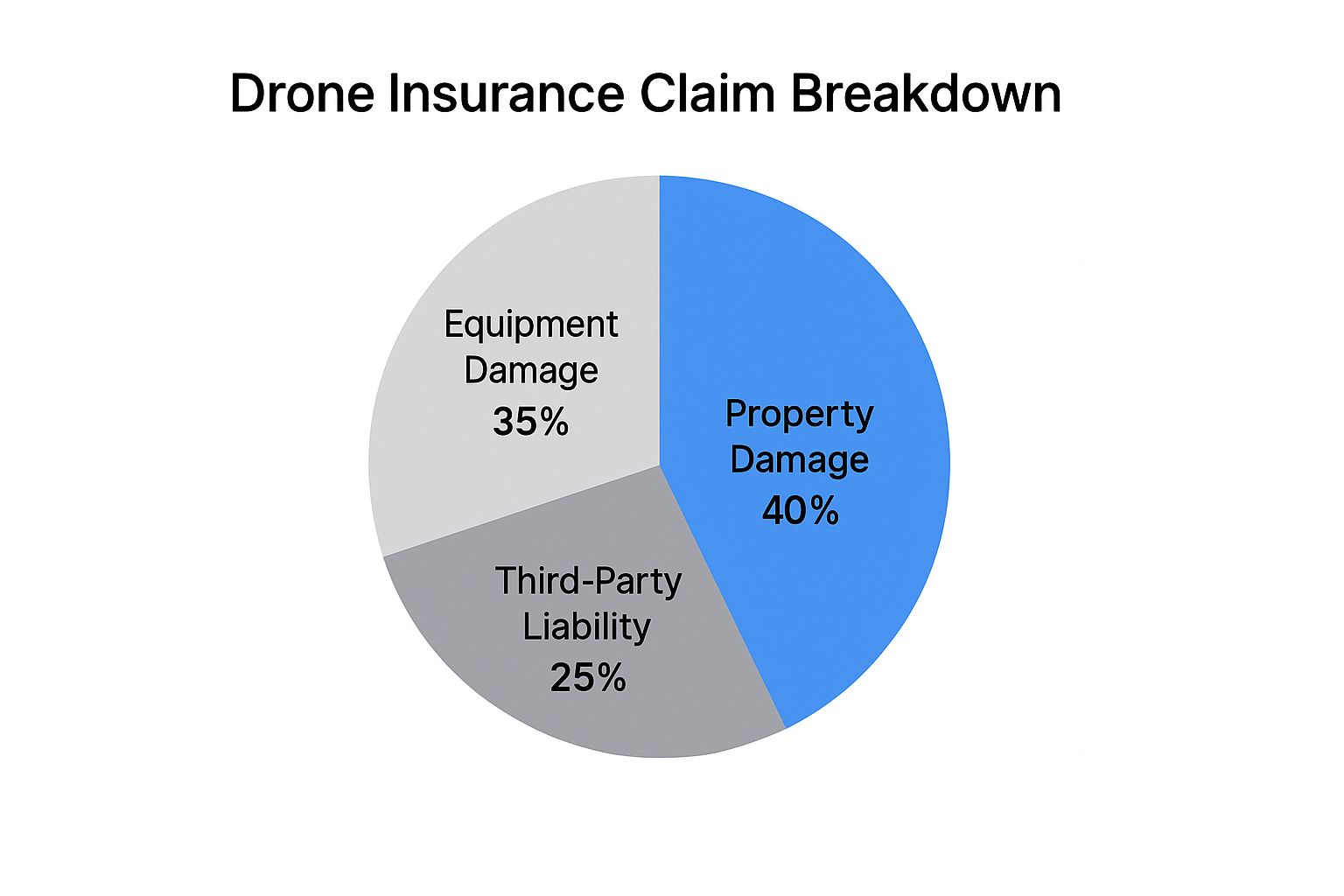

Hull Insurance: This covers damage to your drone itself, much like car insurance. Whether it's a crash, malfunction, or other accident, hull insurance protects your investment in the drone itself.

Liability Insurance: If your drone causes damage to someone or their property, liability insurance protects you financially. This is particularly important when flying in populated areas or near infrastructure. Imagine a scenario where your drone malfunctions and damages a car; liability insurance would step in.

Payload Insurance: For drones carrying specialized equipment like cameras or sensors, payload insurance covers damage or loss to these payloads. This is crucial for businesses investing in expensive equipment for their drones. For instance, if your drone’s camera is damaged during a flight, payload insurance can help with replacement costs.

Ground Equipment Insurance: This covers the ground-based equipment used to operate your drone, such as the controller or base station.

Matching Insurance to Your Operations

Just as every flight is different, every drone business has unique insurance needs. This is especially true in the rapidly evolving drone industry. In fact, the drone insurance market is projected to reach $2.33 billion by 2029, growing at a CAGR of 10.3% between 2025 and 2029. This growth is driven by increased commercial drone usage and a growing emphasis on mitigating risks. Find more detailed statistics here. This highlights the growing importance of drone insurance in the commercial sector. Choosing the right coverage requires careful consideration of your specific operations.

Consider these scenarios:

Aerial Photography for Real Estate: Liability and hull insurance are essential. Payload insurance for your cameras is also highly recommended.

Infrastructure Inspection: High liability limits are crucial, along with hull and payload insurance for sensors.

Agricultural Mapping: Hull insurance and coverage for specialized sensors are key. Liability insurance needs may vary based on location and flight paths.

You might be interested in: Our blog post sitemap for more information. By analyzing your operational risks, you can ensure you have the right coverage without paying for unnecessary extras. Understanding your needs allows you to tailor your insurance policy to your business perfectly. This proactive approach ensures your drone operations are properly protected so you can focus on growth.

Navigating the Regulatory Maze With Confidence

Drone business insurance is more than just protecting your equipment. It’s about successfully navigating the complex world of drone regulations. These regulations, which exist at the federal, state, and even local levels, can have a significant impact on your operations.

Understanding these rules is key to maintaining proper insurance coverage and avoiding legal problems. This is especially important for commercial drone operators, where the financial and legal stakes are often much higher.

Understanding FAA Mandates

At the federal level, the Federal Aviation Administration (FAA) establishes the core rules for drone operation. Complying with these regulations is mandatory for all drone pilots, regardless of whether they are flying for recreational or commercial purposes. Drone business insurance policies frequently require proof of FAA compliance, such as holding a Part 107 certificate for commercial operations.

This certification proves that a pilot understands the knowledge and safety standards established by the FAA. Maintaining good documentation, including flight logs and maintenance records, is also essential for demonstrating compliance and ensuring your insurance remains valid.

Addressing Local Ordinances

Federal regulations provide a foundational framework. However, state and local ordinances add another layer of complexity. These local rules can vary widely, covering things like permitted flight zones, altitude restrictions, and even noise levels.

For instance, one city might prohibit drone flights over public parks, while another might have specific regulations about nighttime operations. Ignoring these local ordinances can lead to fines, legal issues, and potentially invalidate your drone business insurance coverage. So, it's essential to research and understand the rules in each location you operate.

Insurance Credentials for Different Operations

The insurance credentials you need can differ based on the kind of drone operation you are carrying out. Standard commercial flights might require a certain level of liability coverage, while specialized operations, like infrastructure inspection or aerial cinematography, could demand higher limits and additional protections.

This means drone businesses need to adjust their insurance coverage to match the different risk profiles of various jobs. Flexibility in your drone business insurance policy is vital for ensuring proper protection for every operation.

International and Cross-Border Operations

For businesses engaged in international or cross-border drone operations, the regulatory environment becomes even more challenging. Each country has its own unique drone laws and insurance requirements. Navigating these international regulations requires careful preparation and potentially specialized insurance solutions. Failing to comply with international regulations can result in significant legal and financial penalties.

Visualizing Drone Insurance Requirements

The following data chart visualizes minimum liability coverage amounts required for different commercial drone operations across three hypothetical regions (A, B, and C). These amounts, ranging from $500,000 to $2,000,000, show the broad range of liability requirements drone businesses might encounter.

Operation Type | Region A | Region B | Region C |

|---|---|---|---|

Aerial Photography | $500,000 | $750,000 | $1,000,000 |

Real Estate | $500,000 | $1,000,000 | $1,500,000 |

Infrastructure Inspection | $1,000,000 | $1,500,000 | $2,000,000 |

Industrial Applications | $750,000 | $1,250,000 | $1,750,000 |

Region A consistently has the lowest minimums, while Region C has the highest, suggesting a stricter regulatory environment. The chart also highlights that aerial photography and real estate operations typically require less coverage than infrastructure inspection or industrial applications. This difference emphasizes the perceived higher risk associated with operating near critical infrastructure or in complex industrial settings.

By understanding and adapting to these diverse regulations, drone businesses can operate with confidence and within the law, ensuring their insurance provides truly effective protection.

Decoding the Factors That Drive Your Insurance Costs

Securing drone business insurance is essential for any aerial operation. Understanding how premiums are calculated can be confusing, so let's break down the key factors that influence your drone business insurance costs. This information, gleaned from insurance underwriters and seasoned drone pilots, will help you make smart choices about your coverage.

Beyond the Basics: Drone Value and Flight Operations

The value of your drone is a significant factor in your insurance costs, much like insuring a car. A higher-value drone will usually mean higher hull insurance premiums. But it's not just about the drone itself. Your flight environment matters too.

Operating in busy urban areas presents more risk than flying in open rural spaces, potentially increasing your liability premiums. This is because of the increased chance of accidents and property damage in congested areas.

The type of work you do also makes a difference. Simple aerial photography usually commands lower premiums than complex industrial inspections. For example, inspecting a cell tower at 200 feet has greater inherent risk than photographing a house from 40 feet.

The Power of Safety: Certifications and Procedures

Your pilot certifications and safety procedures are powerful tools for influencing your insurance costs. Holding certifications like the FAA Part 107 Certificate shows your competence and professionalism, which insurers value.

Think of it as similar to a driver's education course reducing car insurance rates. A certified pilot is often seen as a lower risk, which could mean premium discounts.

Documented safety procedures also play a vital role. A thorough safety manual outlining pre-flight checks, emergency procedures, and maintenance schedules demonstrates a commitment to risk management. These proactive measures can lead to lower premiums.

Leveraging Flight Data and Negotiation Tactics

Beyond these basics, your flight data and safety record can give you a negotiating edge with insurers. Detailed flight logs showing accident-free operations can help you secure lower premiums, much like a clean driving record for car insurance.

Check out our guide on sitemap pages for more information. This data-driven approach can help you get better insurance terms.

The growing commercial drone market also impacts insurance. This market is expected to hit $57.8 billion by 2030, with a CAGR of 7.9%. Discover more insights about the drone market here. This growth makes understanding the factors behind your insurance costs even more critical for success. By understanding these factors, you can manage your expenses and ensure your business is well-protected.

Finding the Perfect Insurance Match for Your Drone Fleet

Choosing the right drone business insurance is crucial, just like selecting the right drone for a specific job. Not all insurance providers offer the same coverage, and understanding the nuances of drone-specific insurance can save you time, money, and future headaches. This requires careful evaluation of potential insurers to ensure they understand the unique risks associated with drone operations.

Specialized Drone Insurers Vs. Generalists

There's a key difference between specialized drone insurance providers and generalist insurers entering the UAV market. Specialized providers often possess a deeper understanding of drone technology, regulations, and the risks involved in various operations. This specialized knowledge can be invaluable when tailoring coverage to your specific needs.

Generalist providers, while possibly offering lower initial premiums, may not fully grasp the specific challenges of aerial operations. This could leave gaps in your coverage when you need it most. For instance, a generalist policy might not cover damage from a flyaway drone, a common scenario addressed by specialized providers.

Decoding Policy Language and Identifying Red Flags

Understanding your insurance policy's details is paramount. Be on the lookout for red flags that might limit coverage during a claim. Some policies exclude coverage for specific payloads or operations, such as beyond visual line of sight (BVLOS) flight. Identifying these exclusions upfront is critical.

Also, pay close attention to the Combined Single Limit (CSL), the total bodily injury and property damage liability coverage. Adequate liability coverage is especially important for commercial drone operations. Imagine a drone malfunction causing property damage or injury – you'll need sufficient coverage to protect your business.

Evaluating Insurer Expertise and Claims Satisfaction

Beyond policy specifics, research the insurer's drone industry expertise. Look for providers with a history of handling drone-related claims efficiently and fairly. Online reviews and industry forums can provide valuable insights from other drone operators. This research offers crucial information about an insurer's reliability and responsiveness.

Financial stability is also key. You need confidence that the insurer can pay out a substantial claim. Check the insurer's financial ratings and reviews to confirm their reliability. A financially sound insurer provides peace of mind, knowing your claim will be handled effectively.

To help you compare different insurance providers, we've compiled the following table:

Top Drone Insurance Providers Comparison

Side-by-side comparison of leading drone business insurance providers' offerings, specialties, and limitations

Insurance Provider | Specialization | Coverage Options | Average Premium Range | Claims Process Rating | Industry Experience |

|---|---|---|---|---|---|

Provider A | Commercial drone operations | Hull, Liability, Payload | $500 - $2000 annually | Excellent | 10+ years |

Provider B | Recreational & small business | Liability, Hull | $200 - $800 annually | Good | 5+ years |

Provider C | Aerial photography & videography | Hull, Liability, Equipment | $700 - $1500 annually | Average | 7+ years |

Provider D | Inspection & surveying | Liability, Hull, Cyber | $800 - $2500 annually | Excellent | 12+ years |

This table provides a simplified example and should not be used as a definitive guide for choosing insurance. Actual providers, offerings, and premiums vary.

As you can see, different providers cater to different needs and budgets. It's important to research each provider thoroughly to find the best fit for your business.

Balancing Coverage and Budget

Finding the right insurance involves balancing coverage with budget. While adequate protection is vital, avoid overpaying for unnecessary coverage. Work with an insurance broker specializing in drone insurance to find cost-effective options. Getting multiple quotes from different providers allows you to compare coverage and pricing for the best value.

By understanding these key considerations, you can choose a drone business insurance policy that provides the necessary protection without overspending. This proactive approach lets you focus on growing your drone business, knowing you're protected against the unique risks of aerial operations.

Cutting-Edge Tech That Slashes Your Insurance Costs

Smart investments in drone technology can significantly reduce your drone business insurance premiums. Insurers recognize and reward businesses that prioritize safety and operational efficiency. This section explores the technologies that can translate to substantial savings.

Collision Avoidance Systems: Your First Line Of Defense

Collision Avoidance Systems (CAS) are crucial for safe drone operations. These systems use sensors and algorithms to detect and avoid obstacles, minimizing crash risks. This proactive approach is highly valued by insurers and often results in lower premiums.

Obstacle Detection: CAS identifies obstacles such as buildings, trees, and power lines, automatically adjusting flight paths for collision avoidance.

Autonomous Emergency Braking: In critical situations, CAS can initiate automatic braking to prevent impact and minimize damage.

Imagine your drone encountering unexpected turbulence near a building. CAS can stabilize the drone and steer it clear of the structure, preventing a costly accident. This added safety protects your equipment and demonstrates your commitment to risk mitigation to insurers.

Flight Logging and Maintenance Tracking: Data-Driven Safety

Detailed flight logs and meticulous maintenance records provide valuable data for insurers to assess risk. Flight logging platforms like AirData UAV record crucial flight data, including altitude, speed, and GPS location, helping insurers understand operational patterns and identify potential hazards.

Maintenance tracking tools ensure your drones are in optimal condition. Regular maintenance reduces malfunction risks and demonstrates a commitment to preventative safety, which can lead to lower premiums.

Geofencing and Autonomous Flight: Enhanced Safety and Control

Geofencing creates virtual boundaries, restricting your drone’s flight area. This is useful for avoiding restricted airspace or sensitive areas, showcasing operational responsibility to insurers.

Autonomous flight safety features, such as automated return-to-home functionality, further enhance safety. If connection is lost or the battery runs low, the drone automatically returns to its designated home point, minimizing flyaway risks. These features can contribute to lower insurance costs.

The drone industry is expanding rapidly, even within the insurance sector itself. The Drones for Insurance market is projected to grow from $1.5 billion in 2023 to $5.8 billion by 2032. Explore this topic further.

Cost-Benefit Analysis: Prioritizing Upgrades

While these technologies offer compelling safety benefits, conducting a cost-benefit analysis before investing is essential. Consider the technology's cost, the potential premium reductions, and the overall ROI.

A high-end collision avoidance system might be worthwhile for complex industrial inspections but unnecessary for a small aerial photography business. Read also: Our event sitemap for more insights.

By prioritizing upgrades valued by insurers, you maximize your return on investment and minimize insurance expenses. These strategic investments enhance safety and demonstrate responsible drone operations, strengthening your position during policy negotiations.

Mastering the Claims Process When Things Go Wrong

Operating a drone business comes with inherent risks. Even minor incidents can significantly impact your operations. Understanding the claims process for your drone business insurance is essential for protecting your investment and minimizing downtime. This section outlines crucial steps to take after an incident to maximize a successful claim.

Immediate Actions After an Incident

The first few hours after an incident are the most critical. Your initial response can dramatically affect your insurance claim's outcome. Here’s what successful drone operators do:

Secure the Scene: If it’s safe, secure the area to prevent further damage or evidence tampering. This is much like securing a car accident scene. Securing the site preserves its integrity for later assessment.

Document Everything: Meticulously document the incident with photos, videos, and detailed written notes. Include the date, time, location, weather conditions, and a thorough event description.

Contact Your Insurer: Notify your insurance provider immediately. Prompt communication shows responsibility and quickly starts the claims process.

Documentation Requirements for Different Claim Types

Different incidents necessitate different documentation. Understanding these specific requirements helps you prepare a comprehensive claim.

Hull Damage: You'll need detailed photos and videos of the drone damage, including repair estimates and purchase receipts.

Liability Claims: Gather information about any third-party injuries or property damage, witness statements, and relevant police reports.

Flyaway Claims: Flight logs, pre-flight checklists, and maintenance records are often necessary to prove proper operational procedures.

For instance, if your drone experiences a flyaway, comprehensive flight logs provided to your insurer can demonstrate you operated within safe parameters.

Preserving Evidence and Strengthening Your Position

Preserving evidence correctly strengthens your claim and helps prevent disputes. Consider these best practices:

Store Data Securely: Back up all flight logs, photos, and videos to prevent data loss. Cloud storage services offer a valuable tool for secure backup.

Maintain Chain of Custody: Document everyone who handled the drone and related evidence after the incident. This is similar to forensic procedures and ensures the evidence’s reliability.

Don't Admit Fault: Avoid admitting fault or speculating about the cause. Let the insurance investigation determine responsibility.

Common Reasons for Claim Denial

Understanding why claims are denied helps you avoid common pitfalls. Some frequent reasons include:

Operating Outside of Policy Coverage: Flying in restricted airspace or engaging in activities not covered by your policy can lead to denial.

Lack of Proper Documentation: Insufficient evidence or incomplete documentation weakens your claim and may cause rejection.

Pilot Error: Claims might be denied if the incident resulted directly from pilot error, particularly if it involved violating FAA regulations.

Undisclosed Modifications: Modifying your drone without informing your insurer could invalidate coverage and lead to a denied claim.

Effective Communication with Adjusters

Clear, professional communication with insurance adjusters is essential for a smooth process.

Be Responsive: Respond promptly to adjuster requests for information or documentation. Timely responses significantly speed up the process.

Keep Records: Maintain records of all communication with the adjuster, including emails, phone calls, and letters. This creates a clear communication trail.

Seek Professional Advice: Consult with an aviation attorney specializing in drone insurance if your claim is complex or disputed.

Maintaining Operations During the Claims Process

Downtime is costly. Planning ahead helps maintain operations during the claims process.

Backup Equipment: A backup drone ensures business continuity if your primary drone is out of service.

Rental Options: Explore renting a drone temporarily while yours is repaired or replaced. This maintains operations without a major investment.

By following these guidelines and understanding drone business insurance claims, you can navigate difficult situations and protect your aerial enterprise. Preparation and proactivity can minimize the impact of incidents and keep your drone business thriving.

Emerging Trends Reshaping Drone Business Insurance

The drone insurance landscape is constantly evolving, driven by technological advancements and the expanding use of drones across various industries. This means drone operators need to understand how these changes impact their coverage needs and the available insurance options. Staying informed ensures your business remains protected and competitive.

The Rise of Autonomous Flight and BVLOS Operations

Autonomous flight and Beyond Visual Line of Sight (BVLOS) operations are transforming the drone industry. As drones become more sophisticated, they can perform complex tasks with minimal human intervention, opening exciting new opportunities for businesses. However, these advancements also present unique insurance challenges.

Increased Complexity: Autonomous systems introduce complexities that traditional insurance models haven't fully addressed. Insurers are developing new ways to assess risk for drones that make independent decisions.

Shifting Liability: BVLOS operations raise questions about liability in scenarios where the pilot can't directly see the drone. This requires updated insurance policies to address potential risks.

For example, a drone autonomously inspecting a wind turbine presents different risks than a manually piloted drone capturing real estate footage. Insurance providers are innovating with policies specifically designed for these emerging applications.

Urban Air Mobility and Its Insurance Implications

Urban Air Mobility (UAM), encompassing air taxis and cargo delivery drones, is poised to revolutionize urban transportation. This shift creates a new market for specialized drone business insurance. The risks associated with operating drones in densely populated areas require tailored coverage and higher liability limits. Imagine a delivery drone malfunctioning and causing damage in a busy city center – robust insurance becomes paramount.

Usage-Based Insurance and Real-Time Risk Assessment

The insurance industry is adopting data-driven approaches to risk assessment. Usage-based insurance, which uses real-time flight data to dynamically adjust premiums, is gaining traction. Think of it like car insurance that tracks your driving habits – safe drone operations can lead to lower insurance costs.

Real-time risk assessment utilizes sensors and data analysis to identify potential hazards during flight. This allows for immediate adjustments to mitigate risks and demonstrate responsible operations to insurers.

Data-Driven Underwriting and Specialized Markets

Data analytics are transforming how insurers evaluate risk. Data-driven underwriting uses flight data, maintenance records, and pilot experience to tailor insurance policies and offer competitive premiums.

Emerging drone applications, like precision agriculture and medical delivery, are creating specialized insurance markets. Providers are developing policies that cater to the specific needs of these industries, offering customized solutions for unique operational risks.

Preparing for the Future of Drone Insurance

To stay ahead, drone businesses should:

Stay Informed: Keep up-to-date on emerging trends and regulatory changes in the drone insurance landscape.

Embrace Technology: Invest in safety technologies that can lower insurance premiums and improve operational efficiency.

Consult with Specialists: Work with insurance brokers specializing in drone insurance to ensure your business has comprehensive and cost-effective coverage.

By understanding these evolving trends and proactively adapting, you can ensure your drone business remains protected and positioned for success in this dynamic market.

Ready to protect your drone operations with comprehensive and innovative insurance solutions? Visit JAB Drone to learn more about navigating the complexities of drone business insurance and find the perfect policy for your needs.

Comments